By Keiter CPAs

Who gets the family Bible

When blood is split apart?

Tell me who gets the family bible

When two grownups lose heart?

Rick Logan, “Family Bible” (written by Jon Brion and Adam McKay)

In our previous discussion on valuing marital assets titled “Who Gets the Family Bible? Division of Hybrid Property in Divorce, Part I”, we looked at the Brandenburg and Keeling methods to quantify the separate and marital components of real estate. Now we will look at the Hosier formula which may be more applicable than Brandenburg and Keeling in cases with differing fact patterns.

The Hosier formula, presented in Hosier v. Hosier[1], is also referred to as the Net Percentage Gain formula. The formula is discussed in the appellate court’s memorandum opinion as follows:

Using a consistent meaning for the phrase ″net proceeds,″ the decree starts the calculation of wife’s separate interest with the ″actual net proceeds″ – meaning the gross sale price less the sellers’ transactional costs. This figure would then be compared to the initial purchase price paid by husband and wife to arrive at a ″net gain percentage,″ the home’s appreciation over the term of the marriage. That appreciation percentage would be applied to the wife’s separate contribution of $19,159, giving it exactly the same return on investment she would have had if she had purchased another asset worth $19,159 with a similar appreciation in value.

The trial court returned wife’s separate interest with the same percentage increase enjoyed by the total investment, thus recognizing wife’s role in purchasing the asset. The marital interest in the home likewise received the benefit of market appreciation, thus recognizing the costs associated with holding the investment (a precondition to its appreciation) during the term of the marriage — including debt maintenance, which is mostly interest in the early stages of the amortization schedule, as well as durational costs like insurance premiums and real estate taxes. In this way, the trial court’s methodology prudently balanced the financial expectancies related to capital acquisition costs (supported entirely by wife’s separate interest) and asset retention costs (supported entirely by marital interests).[2]

The Hosier formula can be presented as follows:

NG% = NP / PP

SI = SC x NG%

MI = NP – SI – D

Where:

NG% = Net gain percentage

NP = Net proceeds, calculated as gross sales price less transaction costs

PP = Purchase price of subject property

SI = Separate interest in subject property

SC = Separate contribution to acquire subject property

MI = Marital interest in subject property

D = Net liabilities on the subject property

The Hosier formula, as discussed above, recognizes the importance of the separate contribution to the acquisition of the subject property and applies the percentage increase of the total investment to the separate contribution. Additionally, the Hosier formula allocates value to the marital interest for the cost of retaining the subject property, even when the debt balance associated with the subject property increased, which is especially helpful in an era of zero interest-rate policies and interest-only loans.

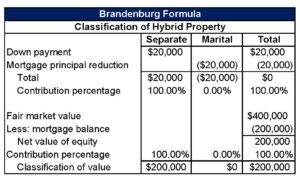

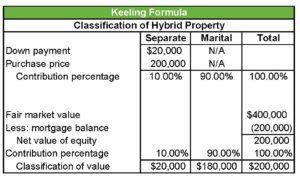

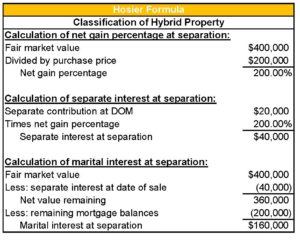

The difference between Brandenburg, Keeling, and Hosier can be illustrated by the following example. Mr. and Mrs. Smith are married on January 1, 2XX1, and buy a house that day for $200,000. Mrs. Smith puts down $20,000 and the couple takes out a mortgage for the remaining $180,000. A few years later, the Smiths make an addition on the house and take out an additional $50,000 to finance it. Several years later, Mr. Smith goes to Washington and refuses to leave, leading to the couple’s divorce. When the couple separates on December 31, 2X10, the house has a fair market value of approximately $400,000 and the mortgage has a principal balance of $200,000. Using the Brandenburg, Keeling, and Hosier formulas, the value of the separate and marital components of the couple’s real estate is as follows:

Under the Brandenburg formula, the mortgage balance increased during the marriage so the marital contribution is classified as negative. Consequently, the entire value of the house would be Mrs. Smith’s property despite the fact that the couple were equally responsible for the mortgage during the duration of their marriage. Using the Keeling formula, Mrs. Smith’s initial contribution of $20,000 has grown by 0% in 10 years while the value of the house doubled, resulting in a separate interest of $20,000 and a marital interest of $180,000. The Hosier formula applies the net gain percentage on the house of 200% to Mrs. Smith’s initial contribution of $20,000, resulting in a separate interest of $40,000 for Mrs. Smith at the date of separation and a marital interest of $160,000.

As the examples above show, the calculation of separate and marital interests in real estate can result in a wide range of values depending on the methodology employed. Accordingly it is imperative that the financial expert and attorney work together to determine the appropriate approach given the particular facts and circumstances, venue, and the relevant case law.

[1] Hosier v. Hosier, 2007 Va. App. LEXIS 62, *1-2, 2007 WL 506081 (Va. Ct. App. Feb. 20, 2007).

[2] Hosier v. Hosier, 2007 Va. App. LEXIS 62, *1-2, 2007 WL 506081 (Va. Ct. App. Feb. 20, 2007), 4-5.

About the Author

Keiter CPAs

Keiter CPAs is a certified public accounting firm serving the audit, tax, accounting and consulting needs of businesses and their owners located in Richmond and across Virginia. We focus on serving emerging growth businesses and companies in the financial services, construction, real estate, manufacturing, retail & distribution industries and nonprofits. We also provide business valuations and forensic accounting services, family office services, and inbound international services.

More Insights from Keiter CPAsThe information contained within this article is provided for informational purposes only and is current as of the date published. Online readers are advised not to act upon this information without seeking the service of a professional accountant, as this article is not a substitute for obtaining accounting, tax, or financial advice from a professional accountant.