By Keiter CPAs

It is our goal as tax and accounting advisors to go beyond traditional tax preparation and identify tax savings and planning opportunities for each of our clients. With that in mind, we are sharing an article by Eric Hieber, principal at Winged Keel Group on life insurance in Business Succession planning. We hope you find this article informative and if you would like to learn more about life insurance planning, please contact your Keiter representative or Email | 804.747.0000.

Succession planning for privately held businesses is one of the most popular planning issues in today’s environment. Many owners do not plan adequately, even with growing concerns about how to protect their business for the next generation and with advisors helping them plan for their exit from the business. Business succession planning is emotional, political, time consuming and a distraction from running the day-to-day business. Without proper planning, the results can be disastrous for the business and future generations of the family.

Life insurance plays an important role in any business succession strategy because it is the only asset that provides a lump-sum of cash at a time when it is needed the most – the business owner’s death. Depending on the planning objectives, the life insurance proceeds may be used to meet a variety of funding obligations:

- Fund estate tax liabilities to prevent the business from being sold

- Provide cash to meet the ongoing day-to-day costs of running the business

- Purchase ownership interests from a deceased owner’s estate

In any of these cases, proper life insurance planning can create stability and protection. There are a couple of key strategies utilizing life insurance that can help mitigate the impact of the loss of an owner. Key person insurance, stock redemption plans and buy-sell agreements are specifically designed to help meet these business succession planning issues.

Key Person Insurance

Key person insurance is designed to provide cash to a business to assist with the costs incurred as a result of the death of an owner. Is this scenario, the business is the owner and beneficiary of the life insurance policy. Upon the death of the insured owner, the business receives the death benefit proceeds and uses those assets to meet a variety of objectives, including:

- Cover the day-to-day costs of running the business

- Train or hire a replacement for the deceased owner

- Meet debt obligations of the business

Key person insurance is an asset of the business and the death benefit proceeds would increase the value of the business. The death benefits are received tax-free by the corporation and the proceeds are not included in the estate of the deceased owner.

Stock Redemption Plan

At the policy level, stock redemption plans are structured exactly the same as key person insurance. The business is the owner and beneficiary of the policy. The difference lies in the business’ ability to utilize the funds. Under a stock redemption plan, the death benefit is structured to match each owner’s interest in the business. In the event of the death of one of the owners, the death benefit proceeds received by the business are used to purchase, or redeem, ownership interests from the deceased owner’s estate.

In Estate of Blount v. Commissioner and Estate of Cartwright v. Commissioner, the U.S. Court of Appeals ruled that the death benefit proceeds do not increase the value of the business if there is a valid and binding obligation to use the proceeds to buy the deceased owner’s shares. Without a binding redemption agreement, the death benefit proceeds may increase the value of the business negating some of the benefits of the insurance.

There are several advantages to using a stock redemption plan:

- It provides liquidity to the deceased owner’s estate that may be used to pay estate taxes or support the lifestyle of the surviving family members

- The strategy is relatively simple and does not require the business owners to use personal assets to fund the life insurance – all premiums are paid by the corporation

- The business owners do not need to use available gift exclusions to fund the life insurance

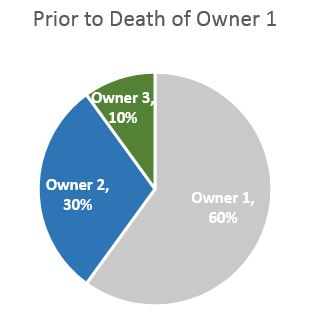

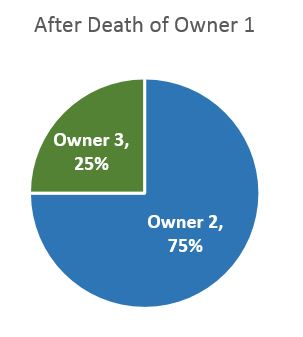

Following the redemption of stock from a deceased owner’s estate, the remaining owners would own 100% of the business based on their pro-rata ownership prior to the death of the deceased owner. The following graphs illustrate how the ownership might look before and after the death of an owner:

Buy-Sell Agreements

The purpose of a Buy-Sell Agreement is essentially the same as a stock redemption plan – to provide cash to a deceased owner’s estate in return for company stock. The Buy-Sell Agreement is different in the ownership of the policies and whom actually buys the deceased owner’s business interest.

In a stock redemption plan, the business purchases the deceased owner’s interest and the remaining ownership is divided amongst the surviving owners on a pro-rata basis. Under a buy-sell agreement, the surviving owners purchase the shares directly from the deceased owner’s estate. The primary benefit of this strategy is the surviving owners receive an increase in their cost basis for the purchase.

Here is how it works. Each owner in the business purchases a life insurance policy insuring the other owners with a death benefit equal to the amount of the business interest the surviving owner would purchase. If there are two owners and they own the business 50/50, they would each purchase a life insurance policy insuring the other owner with a death benefit equal to 50% of the value of the business. Upon the death of an owner, the surviving owner uses the death benefit proceeds to purchase shares from the deceased owner’s estate.

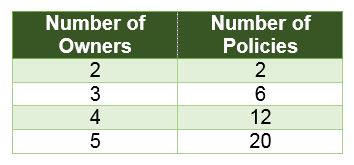

Receiving cost basis for the purchase is beneficial, especially if it is likely the business would be sold following the death of an owner. One drawback to the buy-sell strategy is the number of policies needed to fund the program. As illustrated in the following table, the more owners there are, the more policies are needed and it may not be feasible to administer the plan with more than 3 or 4 owners.

Summary

Liquidity upon the death of a business owner can be the difference between providing meaningful value to surviving owners and family members or seeing an asset that took a lifetime to build deteriorated to meet various funding needs. The benefits of life insurance are uniquely structured to provide the liquidity needed to ensure a successful transition of the business upon the death of an owner.

As with any planning strategy, it is important that the entire advisor team be involved in the process of implementing a life insurance strategy for business succession purposes. Discussions should address the purpose of the insurance, ownership and how the premiums will be paid. With the help of an engaged advisory team, business owners can implement a business succession strategy to maximize the value of the business they have created.

……………………

About Winged Keel

Winged Keel Group (“Winged Keel”) is an independent life insurance brokerage firm founded in 1989 that specializes in the structuring and long-term administration of large life insurance portfolios for ultra-affluent families. www.wingedkeel.com.

Based in the firm’s Richmond and Washington D.C. offices, Eric oversees case design and the management of client relationships. He specializes in structuring customized insurance solutions that assist families and their advisors in their wealth accumulation, wealth transfer, and business succession planning.

About the Author

Keiter CPAs

Keiter CPAs is a certified public accounting firm serving the audit, tax, accounting and consulting needs of businesses and their owners located in Richmond and across Virginia. We focus on serving emerging growth businesses and companies in the financial services, construction, real estate, manufacturing, retail & distribution industries and nonprofits. We also provide business valuations and forensic accounting services, family office services, and inbound international services.

More Insights from Keiter CPAsThe information contained within this article is provided for informational purposes only and is current as of the date published. Online readers are advised not to act upon this information without seeking the service of a professional accountant, as this article is not a substitute for obtaining accounting, tax, or financial advice from a professional accountant.