The IRS and Virtual Currency Transactions

An estimated 46 million Americans have purchased or otherwise been engaged in some type of virtual currency transaction and the IRS believes a far fewer number are reporting those transactions and paying taxes on the income generated. As such, virtual currency has become a hot topic within the IRS and enforcement and collection efforts have begun in earnest.

If you’re a high income earner engaging in virtual currency transactions (Bitcoin, Litecoin, Dash, etc.), we have provided some basic information below to help you understand what your reporting responsibilities are as a United States taxpayer.

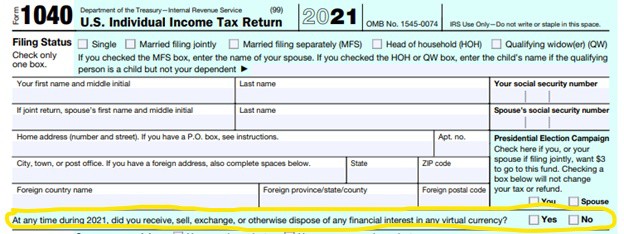

IRS 1040 Virtual Currency Transaction Checkbox

For the last couple of years, the IRS has included a question on the first page of the Form 1040 that asks whether you have purchased or sold virtual currency. The wording of the question has changed slightly each year, but for 2021 this is what you will expect to see – front and center – just below your name and address information:

You must check the box “Yes” if you were involved in any of the following transactions in 2021:

- You received virtual currency (VC) as payment for goods or services

- You received VC as a result of mining, staking, hard fork, or yield farming

- You received VC for free (without providing any consideration) that does not qualify as a gift

- You exchanged VC for property, goods or services

- You exchanged VC for another VC (i.e. bitcoin for ether)

- You sold VC or engaged in any other disposition of a financial interest in VC

You do not need to check the box “Yes” if you were involved in these transactions during 2021:

- You simply held VC in a wallet or account or transferred VC from one wallet/account you control to another wallet/account you control

- You purchased VC only

It is important to note that the IRS considers virtual currency as “property” (think stocks and securities) not as “currency”. The treatment of virtual currency as property has major implications for those engaging in virtual currency transactions. The following table provides a brief summary of the taxable implications for a select group of VC transactions. Please note that the taxation of virtual currency is complex. The following is meant to be a guide, but please reach out to your Keiter professional for additional information as it relates to your specific involvement.

| Transaction | Tax Treatment |

|---|---|

| Purchase | Not a taxable event. Purchase price, including commissions and fees = tax “basis” |

| Sale – if an investor | Capital gain treatment |

| Mining | Treated as ordinary income at time of receipt. Potentially subject to self-employment tax |

| Staking | Treated as ordinary income at time of receipt. Potentially subject to self-employment tax |

| Exchange of VC for another VC | Sale of one currency (capital gain) and then purchase of another. Basis = Purchase price as per above. |

| Spending VC (i.e. using VC to buy goods or services) | Treated as Sale = Capital gain treatment |

| Compensation | Ordinary income subject to worker classification rules: W2 reporting or Form 1099 (self-employment tax may be applicable) |

| Hard Fork (no new crypto currency received) | Not a taxable transaction |

| Hard Fork (new cryptocurrency received) | Taxable event = Fair Market Value of new cryptocurrency at the time it is recorded on the distributed ledger |

| Donation of VC to qualified charity | Tax deduction based on FMV if held more than 1 year or tax deduction is cost basis if held less than 1 year |

| Gift of VC | Not a taxable event - potential gift tax reporting requirement generally with carryover basis to the recipient |

Because each “use” of virtual currency or exchange of virtual currency for another virtual currency is a sale for tax reporting purposes and because most sales are fractional interests, it is important for taxpayers to properly track basis and determine holding period. For some taxpayers, there can be hundreds or thousands of sales annually. We strongly recommend that you use a third party to track your purchases, basis and sales transactions. These services will upload directly from the virtual currency platform and have the ability to pull in historical data. These services will generate the tax reporting schedules that can be used for the filing of Schedule D in your income tax return. Examples of such services include:

- https://cointracker.io/

- https://taxbit.com

- https://cryptotrader.tax/

-

Keiter is providing these for informational purposes only and not recommending one service over another. You should perform your own due diligence before choosing a service provider.

-

To date the IRS has issued little guidance on virtual currency. Following are links to what has been issued. Please refer back to the FAQ frequently as the IRS seems to add information to this site as compared to more formal rulings.

- IRA Notice 2014-21 (general description of virtual currency and the determination of taxation pursuant to “property” rules

- IRS FAQ (updated periodically by the IRS)

- Rul. 2019-24 (discussion of taxation as a result of a hard fork)

Consequences of Not Reporting Virtual Currency Transactions

The IRS is serious about virtual currency as demonstrated by putting the question about your VC involvement front and center at the top of Form 1040. In a November 2021 conference, IRS officials stated that they would consider non-reporting and/or the failure to correctly answer the question on Form 1040 as a criminal matter vs a civil tax matter. This treatment is very similar to the non-reporting of foreign bank and investment accounts which saw many taxpayers caught off guard with high penalties and, potentially, jail time.

Keiter Client Information

Please note that Keiter will not be able to generate a tax gain/ loss schedule from a virtual currency transaction listing (ex: excel spreadsheet). Keiter will require a summarized gain/loss schedule from a service that will fully consider all virtual currency transactions and accurately report/track basis.

Please reach out to your Keiter Opportunity Advisor for assistance in sorting through the virtual currency rules as they are ever changing and expanding to be sure that you have the needed documentation to properly report virtual currency transactions.

About the Author

Ginny Graef, CPA, Partner

Ginny enjoys working closely with her clients and their team of legal and financial advisors to provide tax planning solutions that meet her clients’ specific needs and goals. Ginny’s areas of expertise include income, gift, and trust and estate compliance and planning services. In addition, she focuses on compliance and consulting related to investment partnerships.

More Insights from Ginny GraefThe information contained within this article is provided for informational purposes only and is current as of the date published. Online readers are advised not to act upon this information without seeking the service of a professional accountant, as this article is not a substitute for obtaining accounting, tax, or financial advice from a professional accountant.